See also

31.01.2025 08:17 AM

31.01.2025 08:17 AM

US stock markets closed higher on Thursday despite a turbulent trading session that saw investors trying to make sense of mixed corporate earnings. The indices were supported by optimistic statements from Tesla (TSLA.O), which helped offset the negative impact of a weak forecast from Microsoft (MSFT.O).

The market briefly lost ground toward the end of trading after US President Donald Trump announced the possible introduction of 25% tariffs on imports from Mexico and Canada. These two countries are key trading partners of the United States.

The head of the White House clarified that a final decision on tariffs, including possible restrictions on oil supplies from Canada and Mexico, will be made by the end of the day. If approved, the tariffs will take effect as early as February 1.

Investors fear that such measures could increase inflationary pressures and affect US economic growth, adding uncertainty to the markets.

Experts warn that the administration's trade and tax decisions could have a serious impact on the trajectory of the stock market.

"Until there is clarity on tariff and fiscal policy, it will be difficult for investors to determine a sustainable direction," said Oliver Pursche, senior vice president at Wealthspire Advisors.

However, he added that volatility is likely to persist, but will remain within a certain range.

Despite market fluctuations, most sectors of the S&P 500 ended the day in positive territory. The exception was the technology sector (.SPLRCT), while the communications services sector (.SPLRCL) and the financial sector (.SPSY) reached all-time highs.

One of the main growth drivers was Tesla, whose shares jumped by 2.9%. Investors were inspired by Elon Musk's announcement of plans to release more affordable electric vehicles in the first half of 2025. In addition, the company is preparing to test an autonomous taxi service as early as June. The ambitious plans overshadowed Tesla's disappointing quarterly results, which fell short of analysts' expectations.

US stock markets ended the trading session mixed, reflecting investor reactions to the company's earnings reports. While Tesla and Meta (banned in Russia) helped drive gains, Microsoft came under pressure after it issued a disappointing outlook for its cloud computing business.

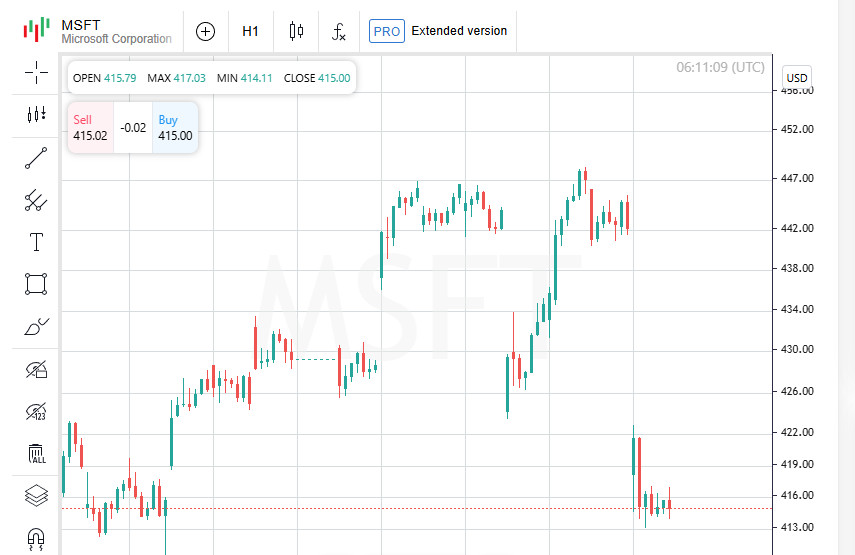

Microsoft (MSFT.O) shares fell 6.2% after the company issued a forecast that disappointed investors. A slowdown in the company's cloud business has raised concerns amid growing competition in artificial intelligence and digital services.

Despite Microsoft's strong position in the cloud segment, its future growth expectations fell short of analysts' estimates, triggering a wave of selling.

Despite pressure from the technology sector, the main US indices ended the day in the green:

The market growth was largely due to positive news from other major players.

One of the growth drivers was the growth of Meta shares (banned in Russia), which rose by 1.6% after the company exceeded revenue expectations for the fourth quarter. However, management warned that sales in the current quarter could be below expectations.

IBM (IBM.N) surprised investors with impressive financial results. The company's shares soared 13%, the largest daily gain since 1999. IBM's quarterly profit was higher than analysts had forecast, which led to a sharp rise in the price of its securities.

Investors are also watching statements from Microsoft executives as they continue to defend their multi-billion dollar investments in AI. This comes amid a recent technological breakthrough by Chinese startup DeepSeek, which has unveiled a revolutionary low-cost AI model.

The news of DeepSeek's developments has rocked Wall Street and caused a wave of selling in AI-related stocks. However, the US tech giants are confident that their long-term investments in AI solutions will pay off in the future.

On Friday, investors are awaiting the publication of the Personal Consumer Expenditure (PCE) price index for December. This indicator is a key indicator of inflation in the US and may influence the Federal Reserve's further actions on interest rates.

The market is bracing for possible volatility, as any deviations from forecasts may lead to a revision of monetary policy expectations.

The US Federal Reserve on Wednesday kept its key interest rate unchanged, reaffirming its cautious approach to future monetary policy changes. Fed Chairman Jerome Powell stressed that further decisions will depend on macroeconomic indicators, including inflation and employment.

The current earnings season has been generally positive for US companies. According to LSEG, more than 70% of S&P 500 companies reported earnings for the fourth quarter of 2024, and most figures exceeded analysts' forecasts. This factor partially offset investor concerns related to monetary policy and slowing economic growth.

However, not all companies were able to please the market.

Logistics giant United Parcel Service (UPS.N) presented a weak forecast for 2025, expecting revenue below market expectations. The news triggered a massive sell-off in the company's stock, with the stock plunging 14.1%, putting pressure on the Dow Jones Transportation Average (.DJT).

UPS's earnings and revenue declines have investors wondering about global demand for shipping and freight, especially as the Chinese and European economies slow.

Apple (AAPL.O) shares fell about 1% in after-hours trading, despite beating analysts' estimates for quarterly profit. The negative reaction was due to weak iPhone sales and lower revenue in China during the holiday season.

The signal could indicate that the smartphone market is becoming saturated, as well as the effects of economic problems in China that are hampering the growth of major tech companies.

Despite some negative news, the overall sentiment in the market remained positive:

Trading volume on U.S. stock exchanges amounted to 13.79 billion shares, which is below the average of 15.4 billion over the past 20 trading days.

This figure indicates moderate demand and caution from investors, who continue to evaluate the impact of global economic factors, corporate reports and upcoming Fed decisions.

Markets remain on the lookout for more data on inflation and consumer spending in the US, which could influence the Fed's future decisions and, consequently, the trajectory of stock indices in the coming weeks.

European stock markets entered a cautious phase of trading on Friday, as investors awaited US President Donald Trump's final decision on import tariffs for Mexico and Canada. With just one day to go until the official announcement, market participants are assessing the possible impact of the move on the global economy.

Amid ongoing uncertainty, the currencies of Mexico and Canada are showing weakness, approaching weekly lows. Investors are concerned that new tariffs from the US could put serious pressure on the economies of both countries, which are important trading partners of the US.

Meanwhile, European stock markets are also showing caution, with EUROSTOXX 50 futures down 0.15% in Asian trading, signalling a grim start to the trading day in Europe.

Amid global uncertainty, the Japanese yen emerged as one of the most resilient currencies in January, rising steadily to post its best monthly performance in seven years. The main driver of the yen's strength remains expectations that the Bank of Japan will continue to tighten monetary policy this year, despite a broader global trend toward easing rates.

Investors see the Japanese currency as a safe haven, especially as the US and other major economies grapple with trade and geopolitical risks.

On Thursday, the US President reiterated his tough trade policy, threatening 100% tariffs on BRICS countries. The move is seen as a warning against possible moves by these countries to replace the US dollar as the dominant reserve currency.

Trump also said he is seriously considering imposing new tariffs on China as early as Saturday. If implemented, these measures could hit the Chinese economy and overshadow the Lunar New Year celebrations, which are considered one of the most important holidays in the country.

All these events are creating a tense atmosphere in financial markets. Investors are waiting for key decisions that could affect global trade, exchange rates and economic growth in the coming months.

Many market participants prefer to take a wait-and-see attitude, assessing possible scenarios for the development of events and their consequences for the global economy.

In addition to the uncertainty around trade tariffs, global markets will be closely watching inflation figures in Germany and France on Friday. These preliminary data could affect investor sentiment and adjust expectations about further actions by the European Central Bank (ECB).

Amid a weakening eurozone economy and progress in the fight against inflation, the ECB left the door open to further interest rate cuts on Thursday. This was a signal to markets that the easing policy in Europe is not over yet.

Later on Friday, the US PCE price index for December, a measure of inflation that the Federal Reserve uses to guide its rate decisions, is due out.

The report could give investors a hint about the future direction of the Fed's monetary policy. However, unless the data shows a significant decline in inflation, the Fed is likely to maintain a cautious approach and not rush to cut interest rates.

The Fed's policymakers signaled earlier this week that they are prepared to maintain a patient strategy, preferring to carefully assess macroeconomic indicators before changing course.

In recent weeks, it has become clear that the world's major central banks are beginning to diverge in their strategies.

This divergence in central bank policies is setting new benchmarks for global markets, creating potential disruptions in capital flows and currency fluctuations.

The current week ends amid a host of uncertainties:

Investors remain in a wait-and-see mode, analyzing macroeconomic indicators and bracing for volatility in the coming days.

You have already liked this post today

*The market analysis posted here is meant to increase your awareness, but not to give instructions to make a trade.